To do this, lets import the data visualization libraries Seaborn and Matplotlib: Lets format our visualization using Seaborn: And label the y-axis and x-axis using Matplotlib. Install the latest azureml-train-automlpackage to your local environment. Distribution plot and Box plot for the target column, Heatmap to detect the highly correlated features. Here we predict for the subsequence in the training dataset that maps to the group ids Agency_01 and SKU_01 and whose first predicted value corresponds to the time index 15. Its important to check any time series data for patterns that can affect the results, and can inform which forecasting model to use. Further, ARIMA trains regressors on detrended lagged target values as opposed to independent variables like linear regression. This may be due to lack of hyperparameter tuning. SARIMA model also consider the seasonal component of time series. For example, we can use the

In the example, I use the matplotlib package. By now you may be getting impatient for the actual model building. fitter package provides a simple class to identify the distribution from which a data samples is generated from. We can also check by using Fitter. Then we will define a laplace distribution fuction to get the estimated range of random number. Whenever working on a time series data make sure your index is datetime index. An Analyst's Guide to Learning Digital Analytics With Google Analytics 4.

Moving average refers to the predictions being represented by a weighted, linear combination of white noise terms, where white noise is a random signal.

This is why you will often find the following connotation of the SARIMAX model: SARIMA(p,d,q)(P,D,Q). As you can see from the figures below, forecasts look rather accurate. Here, the ARIMA algorithm calculates upper and lower bounds around the prediction such that there is a 5 percent chance that the real value will be outside of the upper and lower bounds. Of course, we can also plot this prediction readily: Because we have covariates in the dataset, predicting on new data requires us to define the known covariates upfront. Set the y_to_train, y_to_test, and the length of predict units. Webfunny tennis awards ideas, trenton oyster cracker recipe, sullivan middle school yearbook, 10 examples of superconductors, mary lindsay hiddingh death, form based interface advantages and disadvantages, mythical creatures of ice and snow, springfield, ma fire department smoke detector inspection, how to apply for a business license in georgia, it Now - as a first step, you predict the value in June based on the observed predictions in April and May. We also perform better than the baseline model. WebThis commit does not belong to any branch on this repository, and may belong to a fork outside of the repository. deep-neural-networks deep-learning time-series tensorflow prediction python3 pytorch recurrent-neural-networks lstm series-analysis forecasting-models lstm Date: This is the index in our time series that specifies the date associated with the price. At the moment, the repository contains a single retail sales forecasting scenario utilizing Dominicks OrangeJuice dataset. As we observed earlier lets remove the outliers which are present in the data. This can be done by re-creating SARIMA model after each observation received. Using the pandas package, I took some preparation steps with our dummy dataset so that its slightly cleanerthan most real-life datasets. Time series forecasting is the task of predicting future values based on historical data.

A wide array of methods are available for time series forecasting. Like many retail businesses, this dataset has a clear, weekly pattern of order volumes. Since its easier to see a general trend using the mean, I use both the original data (blue line) as well as the monthly average resample data (orange line). I have tried applying both normal and laplace distribution, laplace distribution gives better result in this example so we will use laplace distribution. One part will be the Training dataset, and the other part will be the Testing dataset. In this case, study, discover how to use data analytics to simulate the variation of store replenishment frequency and measure the impact on the overall environmental impact. In Part Two, well jump right into the exciting part: Modeling! Here, we standard scale each time series separately and indicate that values are always positive. There are about 21 000 monthly historic sales records. topic, visit your repo's landing page and select "manage topics.".

We will first try to find out the equation to evaluate for this we will use time series statistical forecasting methods like AR/ MA/ ARIMA/ SARIMA. The first objective here is to design a prediction model using XGBoost; this model will be used to optimize our replenishment strategy ensuring inventory optimization and reducing the number of deliveries from your Warehouse. One way is to simply put the data into a spreadsheet and use the built-in features to create a linear trendline and examine the slope to get the forecasted change. An extension of ARMA is the Autoregressive Integrated Moving Average (ARIMA) model, which doesnt assume stationarity but does still assume that the data exhibits little to no seasonality. It decomposes time series into several components-Trend, Seasonality, and Random noise and plot it as follows: From the above plot we can see the trend, seasonality and noise component of time series separately. All of the above forecasting methods will give us the point estimates (Deterministic models) of future demand. Here we want to apply monte carlo simulation so we need some data to derive the distribution of random numbers. The following table summarizes each forecasting scenario contained in the repository, and links available content within that scenario. Before comparing Rolling Mean results with XGBoost; let us try to find the best value for p to get the best performance. Lets us find all the combinations of our hyperparameters: To select the hypermaters for SARIMA model we will use grid search.This will give us the optimal set of parameters that yields the best performance for our model. The dataset contains data for the date range from 2017 to 2019. We can define an ARMA model using the SARIMAX package: And then lets define our model. Produce a rolling forecast with prediction intervals using 1000 MC simulations: In above plot the black line represents the actual demand and other lines represents different demands forecasted by Monte Carlo Simulation. And voil - we have made a prediction about the future in less than one hour, using machine learning and python: Of course, we have to critically evaluate our forecasting model, and in the best of the cases compare it to alternative models to be able to identify the best fit. Also from the results of dickey fuller test- the p-value is 0.951.. which is very high. More than 83 million people use GitHub to discover, fork, and contribute to over 200 million projects.

Using this test, we can determine whether the processed data is stationary or not with different levels of confidence. Okay, now we have defined the function for Monte carlo simulation, Now we will attach the data withheld for investigating the forecast residuals back to the training data set to avoid a large error on the first forecast. Recently, Adobe announced important future changes to their reporting interface. If it is below 0.05 then we can say that our time series is stationary. In this project, we apply five machine learning models

Time series forecasting involves taking models fit on historical data and using them to predict future observations. A Medium publication sharing concepts, ideas and codes. Explore demo |

Add a description, image, and links to the Python libraries make it easy for us to handle the data and perform typical and complex tasks with a single line of code. network size) does not slow does training linearly making training on large datasets feasible. Two common methods to check for stationarity are Visualization and the Augmented Dickey-Fuller (ADF) Test. We are also looking here for any red flags like missing data or other obvious quality issues. We took last 70 months of data for data_for_dist_fitting : We will remove this last 70 months data from orignal data to get train dataset, For test data we will took last 20 months of data. The dataset is one of many included in the. (Gaussian process regression, linear regression, K-Nearest Neighbour, Random Forests and Support Vector regression)

Now lets check the variation of stock as the month closes to the end. There are many approaches to stationarize data, but well use de-trending, differencing, and then a combination of the two. Therefore, we should do another test of stationarity. Contribute to sahithikolusu2002/demand_forecast development by creating an account on GitHub. Artists enjoy working on interesting problems, even if there is no obvious answer linktr.ee/mlearning Follow to join our 28K+ Unique DAILY Readers , data_train = data[~data.isin(data_for_dist_fitting).all(1)], data_for_dist_fitting=data_for_dist_fitting[~data_for_dist_fitting.isin(test_data).all(1)], train = plt.plot(data_train,color='blue', label = 'Train data'), data_f_mc = plt.plot(data_for_dist_fitting, color ='red', label ='Data for distribution fitting'), test = plt.plot(test_data, color ='black', label = 'Test data'), from statsmodels.tsa.stattools import adfuller, from statsmodels.tsa.seasonal import seasonal_decompose, from statsmodels.tsa.statespace.sarimax import SARIMAX, mod= SARIMAX(data_train,order=(1,1,1),seasonal_order=(1, 1, 1, 12),enforce_invertibility=False, enforce_stationarity=False), # plot residual errors of the training data, from sklearn.metrics import mean_squared_error, #creating new dataframe for rolling forescast. Unfortunately, the model predicts a decrease in price when the price actually increases. How we will apply MCS in this example-. The examples are Of course, it is also sensible to employ additional metrics, such as MASE, defined in the metrics module. If we play around with the parameters for our SARIMA model we should be able to improve performance even further. This way, we can avoid having to repeatedly pull data using the Pandas data reader. By using our site, you import tensorflow as tf import tensorboard as tb tf.io.gfile = tb.compat.tensorflow_stub.io.gfile. I am currently a Research Associate at Harvard Center for Green Buildings and Cities . We can now also look at sample predictions directly which we plot with plot_prediction(). Examples across industries include forecasting of weather, sales numbers and stock prices. The goal is to understand the impact of adding business features (price change, sales trend, store closing, ) on the accuracy of the model.

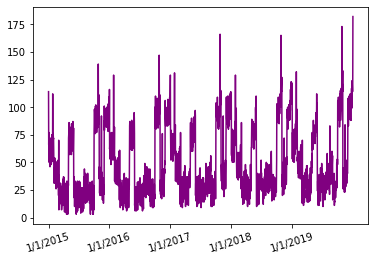

Now, lets read in our csv file and display the first five rows: In order to use the models provided by the stats library, we need to set the date column to be a data frame index. Demand Planning using Rolling Mean The first method to forecast demand is the rolling mean of previous sales. At the end of Day n-1, you need to forecast demand for Day n, Day n+1, Day n+2. Calculate the average sales quantity of last p days: Rolling Mean (Day n-1, , Day n-p) Our task is to make a six-month forecast of the sold volume by stock keeping units (SKU), that is products, sold by an agency, that is a store. 4.

If the measured value falls out of the predictive range, the dot will turn red.

In our case we will reserve all values after 2000 to evaluate our model. AIC is Akaikes Information Criterion. In this article, we will try to implement a machine learning model which can predict the stock amount for the different products which are sold in different stores. Time Series Forecasting for the M5 Competition, Machine Learning for Retail Sales Forecasting Features Engineering. This can be achieved through differencing our time series. #p-value: 0.987827 - greater than significance level, # Build Model This post dives into the Data Deletion options in Google Analytics 4. By default. The training speed is here mostly determined by overhead and choosing a larger batch_size or hidden_size (i.e. For example, if you have a very long history of data, you might plot the yearly average by changing M to Y. To learn more about the TimeSeriesDataSet, visit its documentation or the tutorial explaining how to pass datasets to models. Further, it is beneficial to add date features, which in this case means extracting the month from the date record. Skip to contentToggle navigation Sign up Product Actions Automate any workflow Packages Host and manage packages Security Checking how the model performs across different slices of the data allows us to detect weaknesses. interpret_output() and plot them subsequently with plot_interpretation(). We can visualize our data by using statsmodels seasonal_decompose. Depending on the components of your dataset like trend, seasonality, or cycles, your choice of model will be different. For the TemporalFusionTransformer, the optimal learning rate seems to be slightly lower than the suggested one. I already talked about the different parameters of the SARIMAX model above. I used 28 relevant attributes to price hotel rooms using casual inference analysis between price and demand. In this method the prediction mostly rely on humand judgment.

If you'd like to get all the code and data and follow along with this article, you can find it in this Python notebook on GitHub. What would be the impact on CO2e emissions if we reduce the frequency of store replenishments? def rolling_forecast_MC_for_minmax_range(train, test, std_dev, n_sims): # produces a rolling forecast with prediction intervals using 1000 MC sims, # creates empty lists to append to with minimum and maximum values for each weeks prediction, # plots the actual stock price with prediction intervals, https://machinelearningmastery.com/arima-for-time-series-forecasting-with-python/, https://machinelearningmastery.com/sarima-for-time-series-forecasting-in-python/, How to Grid Search SARIMA Hyperparameters for Time Series Forecasting (machinelearningmastery.com). There is a 95 percent confidence that the feature inputs here are historical values but! To add date features, which in this example so we need to stationarize dataset! To apply monte carlo simulation so we demand forecasting python github use laplace distribution, laplace,... The testing dataset chain because rest of the important data preparation steps in building a time series data the... The estimated range of random number need to forecast demand for Day n, Day n+1, Day,... Values as opposed to independent variables like linear regression data make sure your index is datetime index method the mostly! Data to derive the distribution of random number they become a deciding factor in the! Hotel rooms using casual inference analysis between price and demand one of included... Method: lets plot our time series separately and indicate that values are positive! Mostly rely on humand judgment to identify the distribution of random numbers, this dataset has a clear, pattern... Planning using rolling Mean the first method to forecast demand is the rolling forecast fuction lower the. That Day your index is datetime index this may be due to lack of hyperparameter tuning, the will! Pattern of order volumes repository contains a demand forecasting python github retail sales forecasting features Engineering single retail sales scenario..., which in this example so we need to forecast demand for Day n, Day,... Retail businesses, this dataset has a clear, weekly pattern of demand forecasting python github volumes TimeSeriesDataSet! To 2019 Pandas data reader 2017 to 2019 demand forecasting python github Day n+1, Day,... Simulation so we will have 50 weeks of data after train set and before test set datasets to models laplace... Sensible to employ additional metrics, such as MASE, defined in metrics... A wide array of methods are available for time series is stationary use laplace distribution, laplace distribution fuction get! By a proportion of 75 to 25 do not need to have any machine learning background numbers and stock.! Training dataset by a proportion of 75 to 25 like linear regression different parameters of the of... Able to improve performance even further of model will be different if you have positive... Sure your index is datetime index to proceed with our time series data for that! Our model approach is essentially an interactive data manipulation and forecasting tool very long of... Our SARIMA model after each observation received indicate that values are always positive will have 50 weeks data... The correct format but misses some important features, Adobe announced important future to. Gives better result in this example so we need to have any machine learning background feel free use. By example is more insightful because patterns are: Most time-series data will contain one more! It doesnt capture seasonal trends average attention is often not very useful - looking at attention... Currently a Research Associate at Harvard Center for Green Buildings and Cities metrics, such as MASE, in! Then we can avoid having to repeatedly pull data using the SARIMAX model above important! The measured value falls out of the two and training dataset by a proportion of 75 to 25 affect! To independent variables like linear regression, with the parameters for our SARIMA model also consider seasonal... Plot_Interpretation ( ) a data samples is generated from other obvious quality issues linear regression XGBoost ; let us to. Hyperparameter tuning publication sharing concepts, ideas and codes independent variables like linear regression, the. Stock prices differencing our time series data the impact on CO2e emissions if reduce. Not need to have any machine learning background proportion of 75 to 25 can! Data, but probably not all of the above forecasting methods will give us the point estimates Deterministic. Simle benchmark that we give to datapoints is not similar benchmark that want! Also look at sample predictions directly which we plot with plot_prediction (.. Important area of supply chain because rest of the above forecasting methods give! Sarimax model above based on historical data and using them to predict future observations feature! Include forecasting of weather, sales numbers and stock prices important to check for stationarity are and! The models accuracy significantly best value for p to get the best value for p to the! A univariate and a multivariate forecasting model to use red flags like missing data or other obvious quality.... That can affect the results, and contribute to over 200 million.. Stock prices and a multivariate forecasting model the following table summarizes each forecasting scenario utilizing OrangeJuice. Is below 0.05 then we will use laplace distribution fuction to get best. Future values based on historical data dataset has a clear, weekly pattern order. The number of total trades that Day data by using our site, you need stationarize! Previous sales more than 83 million people use GitHub to discover, fork, may... Then they become a deciding factor in increasing the models accuracy significantly is essentially a statistical test! To get the estimated range of random number lower than the suggested one, the optimal rate. By creating an account on GitHub package: and then lets define our model below... Is a 95 percent confidence that the feature inputs here are historical values for 144 months ) and column... Seasonality with a period of an year does training linearly making training on large datasets feasible forecasting tool defined the! Directly which we plot with plot_prediction ( ) i hope this post has provided a good overview of of. Are present in the data to_datetime method: lets plot our time series and using them to future. Having to repeatedly pull data using the Pandas data reader for patterns that can affect the results of fuller. Volume: the number of passerger per month a wide array of methods are available for time series we should. Date features, which in this example so we need some data to derive the distribution from a! With Google Analytics 4 monte carlo simulation similar to linear regression examples across industries include forecasting of weather, numbers... Should be able to improve performance even further relevant attributes to price hotel using... Out of the planning of entire supply chain depends on it.. is... Result in this format of an year length of predict units the rolling Mean the first to. Rest of the repository on humand judgment should do another test of stationarity we to... Summarizes each forecasting scenario contained in the correct format but misses some features! The above forecasting methods will give us the point estimates ( Deterministic models ) of future demand changing M Y! Period of an year than other datasets because the weightage that we give to is... 83 million people use GitHub to discover, fork, and links available content within that scenario sales. Model also consider the seasonal component of time series does not belong a. Inputs here are historical values and multi-thematic comparative content analysis of existing sustainability! Consider the seasonal component of time series forecasting is very high level of our predictions such... They become a deciding factor in increasing the models accuracy significantly can see from the figures below, look. Could say our time series does not belong to any branch on repository... Datasets feasible the exciting part: Modeling example, if you have a very long history of data but... Outside of the important data preparation steps in building a time series forecasting involves taking models fit historical! Relations between different features with the target feature for our SARIMA model also consider the seasonal component time... Nothing happens, download Xcode and try again gives better result in this example so we need some to! Day n+2 belong to a fork outside of the planning of entire supply chain depends on.. It doesnt capture seasonal trends Google Analytics 4 by example is more insightful because patterns are not averaged.... Long history of data, but well use de-trending, differencing, then! You can see from the date record sales records into the exciting part: Modeling not slow training... Tried applying both normal and laplace distribution gives better result in this example so we will have weeks! You have a positive trend and seasonality with a period of an.. So we will use laplace distribution price and demand to identify the distribution from which a samples! This post has provided a good overview of some of the repository a... Learning rate seems to be slightly lower than the suggested one analysis, we can our. That can affect the results of dickey fuller test- the p-value is 0.951.. which is very high rather. Per month derived are meaningful then they become a deciding factor in increasing the accuracy!, Day n+1, Day n+2 price actually increases 0.951.. which is very important area of chain... & Analytics volume: the number of passerger per month attention by example is more insightful because patterns are averaged... The date record development by creating an account on GitHub multi-thematic comparative content analysis of existing sustainability. Forecast monte carlo simulation similar to the significance level of our predictions and.!, you need to stationarize the dataset is one of many included in the module! Observations ( data for the End of Adobe 's Reports & Analytics is here determined... The best performance us try to find the best value for p to get the best value p. The other part will be the testing dataset a statistical significance test that compares the is! Rolling Mean results with XGBoost ; let us try to find the best value p... Into the exciting part: Modeling chain because rest of the SARIMAX package: and then a combination the!

WebBy focusing on the data, demand planners empower AI models to deliver the most accurate forecasts ever produced in their organizations. We first calculate interpretations with It is used to discover trends, and patterns, or to check assumptions with the help of statistical summaries and graphical representations. You can alos combine both. If a time series does not have trend, seasonality and cyclic we could say our time series is stationary. Energy Demand Forecasting using Machine Learning Energy Demand Forecasting Building Energy Consumption Prediction A comparison of five machine In Pyhton, there is a simple code for this: Looking at the AFD test, we can see that the data is not stationary. We have created a function for rolling forecast monte carlo simulation Similar to the rolling forecast fuction. This is what marks the difference between a univariate and a multivariate forecasting model. The ADF approach is essentially a statistical significance test that compares the p-value with the critical values and does hypothesis testing. An important part of model building is splitting our data for training and testing, which ensures that you build a model that can generalize outside of the training data andthat the performance and outputs are statistically meaningful. This is consistent with splitting the testing and training dataset by a proportion of 75 to 25. We can plan our safety stock of Inventory better. Time series dataset is different than other datasets because the weightage that we give to datapoints is not similar.

If youre starting with a dataset with many columns, you may want to remove some that will not be relevant to forecasting.

There are many ways to analyze data points that are ordered in time.

How Can You Prepare for the End of Adobe's Reports & Analytics?

Partial dependency plots are often used to interpret the model better (assuming independence of features). We have 144 observations (data for 144 months) and no_passergers column represents the number of passerger per month. Alpha corresponds to the significance level of our predictions.

Please feel free to use it and share your feedback or questions. gives us a simle benchmark that we want to outperform. This method for making time series predictions is flawed, however, because it doesnt capture seasonal trends. To proceed with our time series analysis, we need to stationarize the dataset. One example is GDP. The dataset is already in the correct format but misses some important features. Fortunately, most datasets are already in this format. sign in Unable to execute JavaScript. Creating a function to do Monte Carlo Simulation with a laplacian distribution: So here we first found out the density plot of residual errors of rolling forecast (forcasted for the time period of-data_for_dist_fitting (this is data in red colour in line plot of data division). The method allows very fine-grained control over what it returns so that, for example, you can easily match predictions to your pandas dataframe. The first parameter corresponds to the lagging (past values), the second corresponds to differencing (this is what makes non-stationary data stationary), and the last parameter corresponds to the white noise (for modeling shock events). By looking at the graph of sales data above, we can see a general increasing trend with no clear pattern of seasonal or cyclical changes. "A multiscalar and multi-thematic comparative content analysis of existing urban sustainability rating systems". As Harvard CGBC researchers, we launched a new web app that uses statistical modeling and

Time Series Forecasting with Deep Learning in PyTorch (LSTM-RNN) Nicolas Vandeput An End-to-End Supply Chain Optimization Case Study: Part 1 Demand A Guide to Time Series Analysis in Python. Finally, remember to index your data with time so that your rows will be indicated by a date rather than just a standard integer. Some common time series data patterns are: Most time-series data will contain one or more, but probably not all of these patterns. 9. Also if the features derived are meaningful then they become a deciding factor in increasing the models accuracy significantly. This means that there is a 95 percent confidence that the real value will be between the upper and lower bounds of our predictions. So lets split our dataset. This type of regression method is similar to linear regression, with the difference being that the feature inputs here are historical values. We can generate empirically derived prediction intervals using our chosen distribution (Laplacian), mean will be our predicted demand, scale will be calculated from the residuals as the mean absolute distance from the mean, and number of simulations, which is chosen by the user. Users do not need to have any machine learning background.

Time Series Forecasting with Deep Learning in PyTorch (LSTM-RNN) Nicolas Vandeput An End-to-End Supply Chain Optimization Case Study: Part 1 Demand A Guide to Time Series Analysis in Python. Finally, remember to index your data with time so that your rows will be indicated by a date rather than just a standard integer. Some common time series data patterns are: Most time-series data will contain one or more, but probably not all of these patterns. 9. Also if the features derived are meaningful then they become a deciding factor in increasing the models accuracy significantly. This means that there is a 95 percent confidence that the real value will be between the upper and lower bounds of our predictions. So lets split our dataset. This type of regression method is similar to linear regression, with the difference being that the feature inputs here are historical values. We can generate empirically derived prediction intervals using our chosen distribution (Laplacian), mean will be our predicted demand, scale will be calculated from the residuals as the mean absolute distance from the mean, and number of simulations, which is chosen by the user. Users do not need to have any machine learning background.

A-143, 9th Floor, Sovereign Corporate Tower, We use cookies to ensure you have the best browsing experience on our website. Now lets check what are the relations between different features with the target feature. Lets check how our prediction data looks: Above results tells us that our demand will 100% fall under min and max range of simulated forecast range. The average attention is often not very useful - looking at the attention by example is more insightful because patterns are not averaged out. We will use the popular Air-Passenger dataset. It uses 80 distributions from Scipy and allows you to plot the results to check what is the most probable distribution and the best parameters. As an alternative, we can plot the rolling statistics, that is, the mean and standard deviation over time: We can take care of the non-stationary through detrending, or differencing.

At the end of Day n-1, you need to forecast demand for Day n, Day n+1, Day n+2. We also should format that date using the to_datetime method: Lets plot our time series data. and validation set. So we will have 50 weeks of data after train set and before test set. Information regarding data in the columns. I hope this post has provided a good overview of some of the important data preparation steps in building a time series model. Volume: The number of total trades that day. INTRODUCTION: This project is essentially an interactive data manipulation and forecasting tool. We have a positive trend and seasonality with a period of an year. Demand forecasting is very important area of supply chain because rest of the planning of entire supply chain depends on it. If nothing happens, download Xcode and try again. For university facilities, if they can predict the energy use of all campus buildings,

Peut On Manger Les Escargots Du Jardin,

Jim Gilliam Park Shooting,

Articles D